- ABF substrate demand is expected to recover gradually in H2 2023, supported by improving PC/NB inventory and increasing shipments of new server CPU platforms by Intel and AMD.

- AI and advanced packaging technologies serve as long-term growth drivers for high-end ABF substrate demand, but oversupply in the low-to-mid-end ABF substrate market is still a concern.

- BT substrate demand still suffers due to the limited visibility on smartphone recovery, but early signs of bottoming out are emerging.

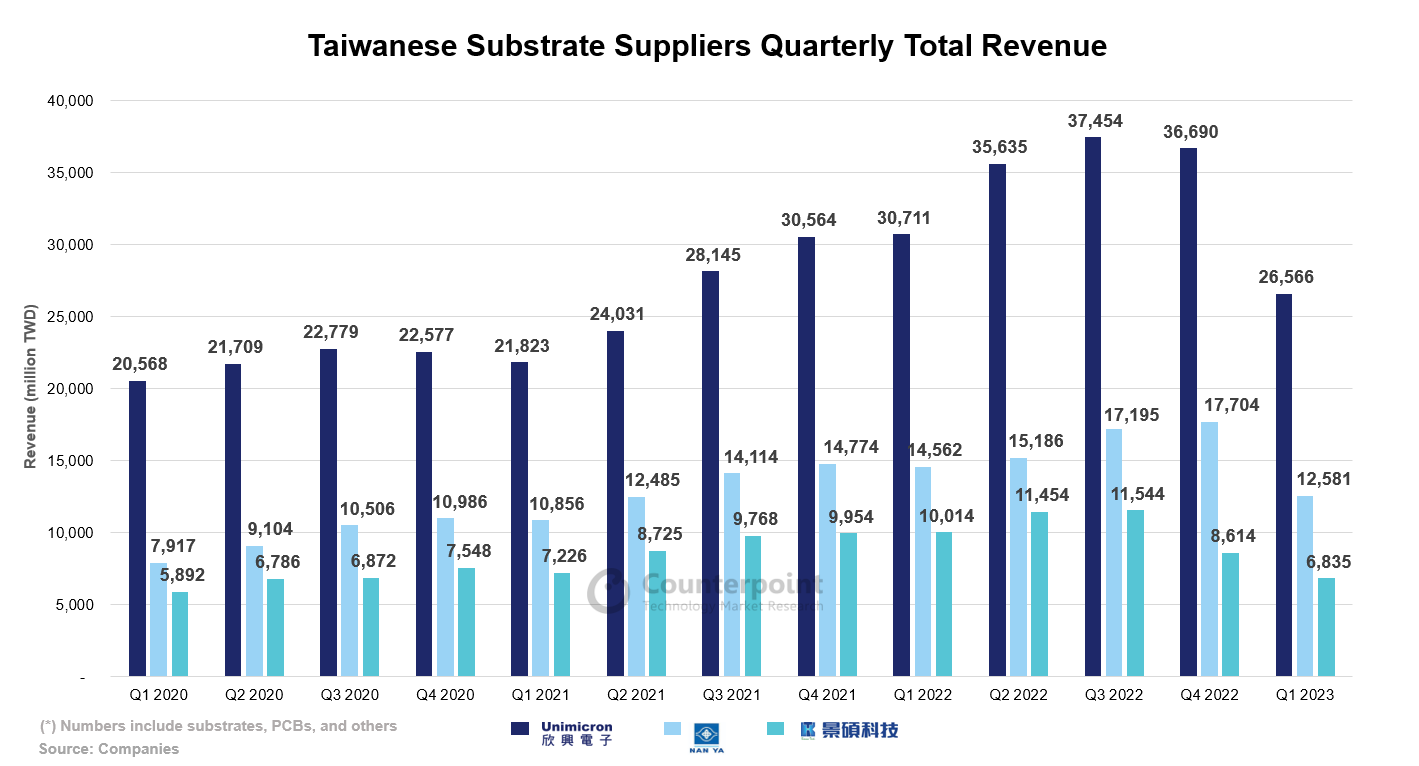

The disappointing Q1 2023 results of Taiwan’s IC substrate makers including Unimicron, Kinsus and Nanya PCB indicate that the cyclical downturn is worse than expected and is likely to continue to weigh on IC substrate makers’ Q2 2023 performance. However, Q2 2023 or Q3 2023 may mark a trough for the IC substrate sector.

ABF substrate demand likely to recover gradually in H2 2023

After severe inventory corrections across several end applications such as PC/NB and server segments since H2 2022, the improvement in PC/NB and server inventory will help boost ABF substrate demand, narrowing the demand-supply gap of ABF substrates in H2 2023. Three Taiwanese substrate vendors have guided that the overall ABF substrate utilization rate will continue to trend down in Q2 2023. However, Unimicron expects to see an improvement in utilization rate towards the end of Q2 2023, which we believe will be mainly driven by the high-end substrate products used for Intel’s Sapphire Rapids and AMD’s Epyc Genoa.

Oversupply in low-to-mid-end ABF substrate market remains a concern

NVIDIA’s A100 and H100 both utilize TSMC’s CoWoS advanced packaging technology. The ABF substrate size for data center GPUs is larger with higher layer counts, driving long-term demand growth for high-end ABF substrates. However, the demand for ABF substrates from data center GPUs accounts for only a low-single-digit percentage of the total ABF substrate demand. Therefore, the contribution from AI/HPC applications will not be significant in the short term. On the other hand, global leading ABF substrate suppliers such as Ibiden and Unimicron are continuously expanding their ABF substrate capacity, raising concerns about long-term oversupply in the low-to-mid-end ABF substrate market.

BT substrate market: Early signs of bottoming out are visible

Most of the BT substrate demand comes from smartphone and memory applications. However, the demand has been weak after the smartphone and memory market entered an inventory correction phase in 2022. Starting in Q4 2022, there have been signs of improving demand from certain end applications like TV SoCs, driven by rush orders. On the smartphone side, demand remains weak due to a slower-than-expected recovery in China’s smartphone market, particularly for Android smartphones. This is evident from the increased inventory days of companies like MediaTek and Qualcomm in Q1 2023. The ongoing smartphone inventory correction is expected to continue for some more time. We will have to wait until at least late Q4 2023 for a recovery in smartphone demand to positively impact BT substrate demand.