- The foundry industry is showing signs of stabilization, marked by a 10% QoQ growth, indicative of ongoing inventory normalization.

- Demand for strong AI remained robust in Q4 2023, setting the stage for continued expansion into 2024.

- The semiconductor inventory cycle is nearing its trough, with demand stabilizing across PC and smartphone applications.

Beijing, Boston, Buenos Aires, Fort Collins, Hong Kong, London, New Delhi, Seoul – Apr 2, 2024

The global foundry industry’s revenue grew about 10% QoQ but fell 3.5% YoY in Q4 2023, according to Counterpoint Research’s Foundry Services. Despite lingering macroeconomic uncertainties, the industry started bottoming out in H2 2023, driven by supply chain inventory restocking demand in the smartphone and PC sectors. Rush orders were observed from both PC and smartphone applications, particularly in the Android smartphone supply chain.

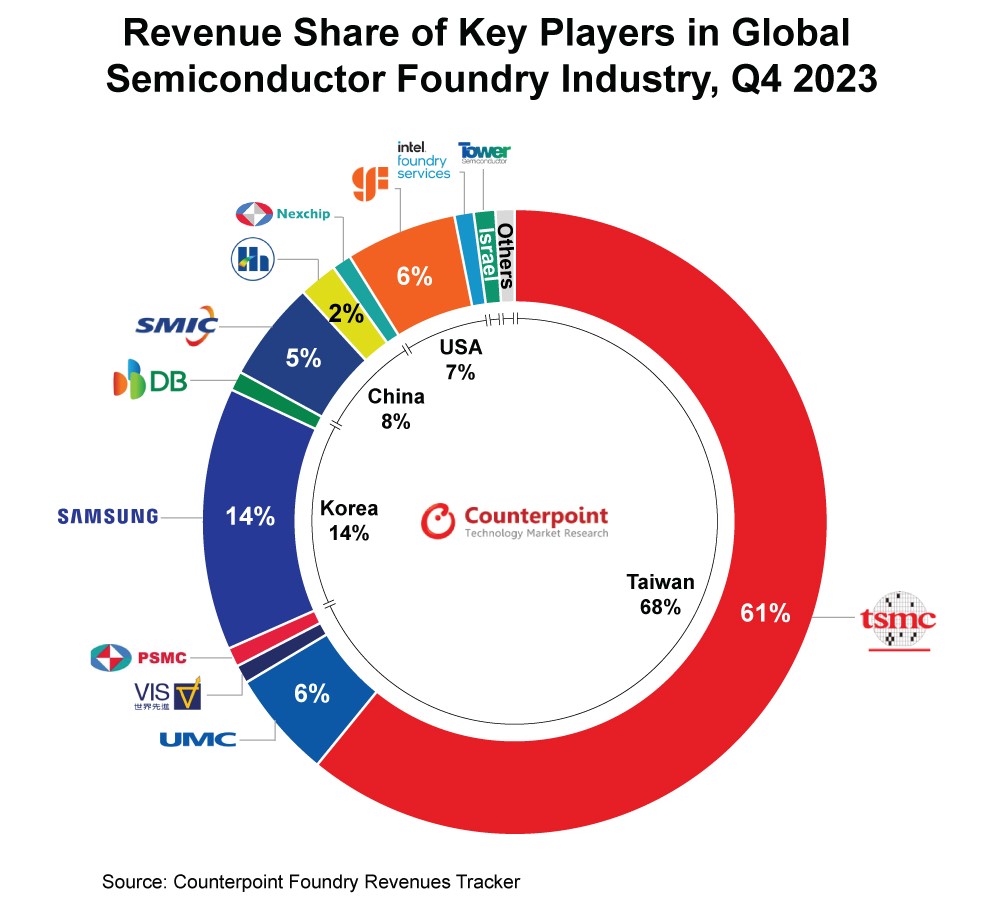

TSMC remained the leader in the foundry industry in Q4 2023, commanding a 61% market share. It posted better-than-expected Q4 2023 revenue, a notable increase from the 59% growth in Q3 2023. TSMC’s 5nm capacity utilization rate reached full capacity, buoyed by robust demand for AI GPUs from NVIDIA. Meanwhile, Apple’s iPhone 15 continued to drive growth in the leading-edge 3nm node. These dual catalysts contributed to revenue from nodes below 7nm, which represented nearly 70% of TSMC’s total revenue for the quarter, underscoring the company’s technology competitiveness.

Counterpoint Analyst Adam Chang commented, “AI demand is expected to remain strong in 2024, with increased capacity from TSMC CoWoS coming online. Simultaneously, the foundry market is very close to the bottom of the semiconductor inventory cycle. TSMC will be the major beneficiary of both the AI mega trend and the logic semiconductor demand recovery.”

Samsung Foundry maintained its second position with a 14% market share in Q4 2023 as smartphone restocking continued during the quarter. The surge in initial pre-orders for the Samsung S24 series bodes well for revenue contribution from Samsung’s 5/4nm.

Among mature node foundries, both GlobalFoundries and UMC delivered better-than-expected results, each holding a 6% market share in Q4 2023. However, both companies provided weak Q1 2024 guidance, largely reflecting poor demand and customer inventory adjustments, especially in automotive and industrial applications. SMIC had a 5% market share in Q4 2023, with 7/10/14nm capacity utilization rates running high to fulfill Huawei Kirin chips and China’s local CPU/GPU demand. SMIC anticipates an increase in rush orders for specific smartphone-related components, including TDDI and CIS, in the near term, but has adopted a cautious full-year outlook due to uncertainties in demand sustainability, echoing the conservative outlook of other mature node foundries.

Following a sharp downturn in 2023, the foundry industry is forecast to return to a growth trajectory in 2024 as inventory continues to normalize. Strong demand for AI and a mild recovery in end demand will serve as the main growth drivers for the industry in 2024.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

![]()

Related Posts