New Delhi, London, Hong Kong, Beijing, San Diego, Denver, Seoul, Buenos Aires – June 7, 2022

Driven by the global premium and mid-tier 5G portfolio, global smartphone AP (Application Processor)/SoC (System on Chip) chipset and baseband revenues grew 23% YoY in Q1 2022, according to the latest research from Counterpoint’s Foundry and AP/SoC service. In Q1 2022, 5G AP/SoC and baseband revenues grew 36% compared to the same period a year ago.

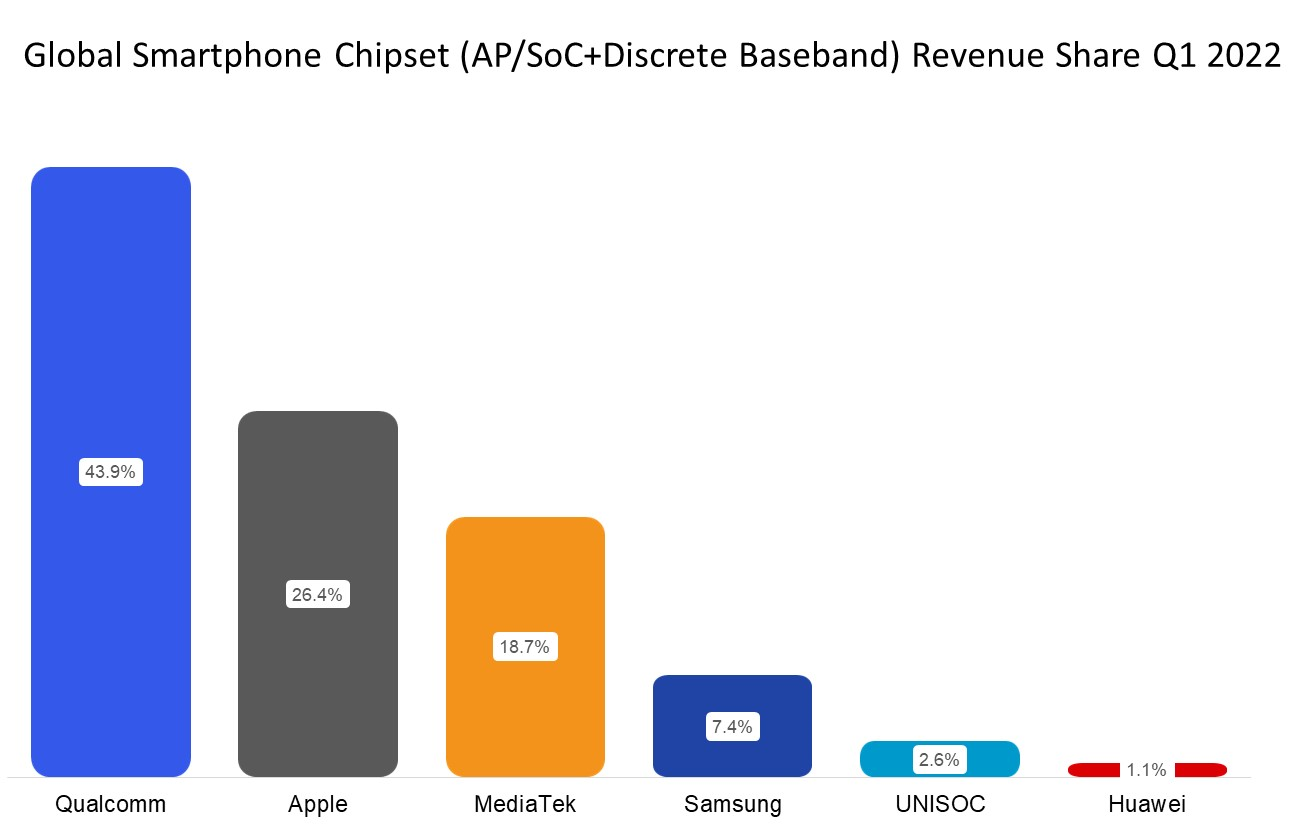

Source: Counterpoint’s Foundry and AP/SoC service

Source: Counterpoint’s Foundry and AP/SoC service

Note: Total revenues include revenues generated from the AP/SoC and discrete baseband

Research Director Dale Gai said, “Qualcomm leads the smartphone AP/SoC and baseband revenues with 44% share. The revenue reached $6.3 billion for Qualcomm, growing 56% YoY in Q1 2022, driven by the higher premium mix which has led to growth in the ASPs. Qualcomm is also providing the discrete baseband shipments to Apple and Qualcomm’s own AP’s, which contribute to around a quarter of Qualcomm’s smartphone AP/SoC and baseband revenues.”

Commenting on the growth in MediaTek’s performance, Senior Analyst Parv Sharma said, “MediaTek’s revenues grew 29% YoY in Q1 2022, reaching a 19% share in global AP/SoC and baseband revenues. MediaTek has dominated the volume shipments for 5G mid-tier smartphones and 4G smartphones. The penetration of 5G is growing continuously and this is helping drive higher revenues for MediaTek. It has also entered the premium 5G segment for the first time with its Dimensity 9000, and this chip, together with the Dimensity 8000, has added impetus to its overall revenues.”

Summary:

Qualcomm: Qualcomm leads the smartphone AP/SoC and baseband revenues with a 44% share. Qualcomm’s revenue grew by 56% YoY in Q1 2022 driven by the higher premium mix which has led to growth in the ASPs. Around a quarter of Qualcomm’s smartphone AP/SoC and baseband revenues are derived from its sales of discrete basebands.

MediaTek: MediaTek captured a 19% share of the total global smartphone AP/SoC and baseband revenues. The AP/SoC and baseband revenues for MediaTek grew 29% YoY in Q1 2022. Driven by the higher 5G ASP and entry into the premium tier with its Dimensity 9000 series.

Apple: With consistent healthy demand for the premium iPhone 13 series, Apple captured the second position with a 26% share. Apple uses Qualcomm’s discrete basebands for 5G connectivity in the iPhone 12 and iPhone 13 series.

Samsung Exynos: Samsung captured fourth position with a 7% share in the AP/SoC and baseband revenues in Q1 2022. Samsung revenue also grew sequentially. Samsung’s shipment volume increased in Q1 2022 due to the launch of Exynos 1280. Samsung launched the Galaxy A33 and A53 with its Exynos 1280 SoCs. However, despite some positive indicators, Samsung Exynos’ share declined in Q1 2022 due to losing share to Qualcomm in the flagship Galaxy S22 series smartphones and due to the low yields of the 4nm premium Exynos chipsets.

UNISOC: UNISOC captured 3% of the overall AP/SoC and baseband revenues. A larger part of the revenues is driven by its 4G AP/SoCs, which have grown significantly over the past years. The share of UNISOC AP/SoC shipments reached 11% in Q1 2022. It has gained share as other chipset providers have focused less on the 4G LTE AP/SoCs creating a shortage of supply that UNISOC took advantage of to win new customers and market share. UNISOC was able to expand its customer base with design wins with realme, HONOR, Motorola, Samsung, ZTE and TECNO all launching phones with UNISOC’s Tiger series of chipsets.

HiSilicon: Affected by the US trade ban, Huawei was unable to manufacture the HiSilicon Kirin chipsets. The accumulated inventory of Kirin SoCs is on the verge of being exhausted. The overall revenues have declined from 8% in Q1 2021 to 1% in Q1 2022.

Please click here to view the full report.

For our comprehensive research on foundry to chipsets to devices, feel free to get in touch with us at the contacts given below.

Analyst Contacts:

Parv Sharma

Dale Gai

Follow Counterpoint Research

press@counterpointresearch.com