Xiaomi Faces Headwinds Globally in Q3 2022

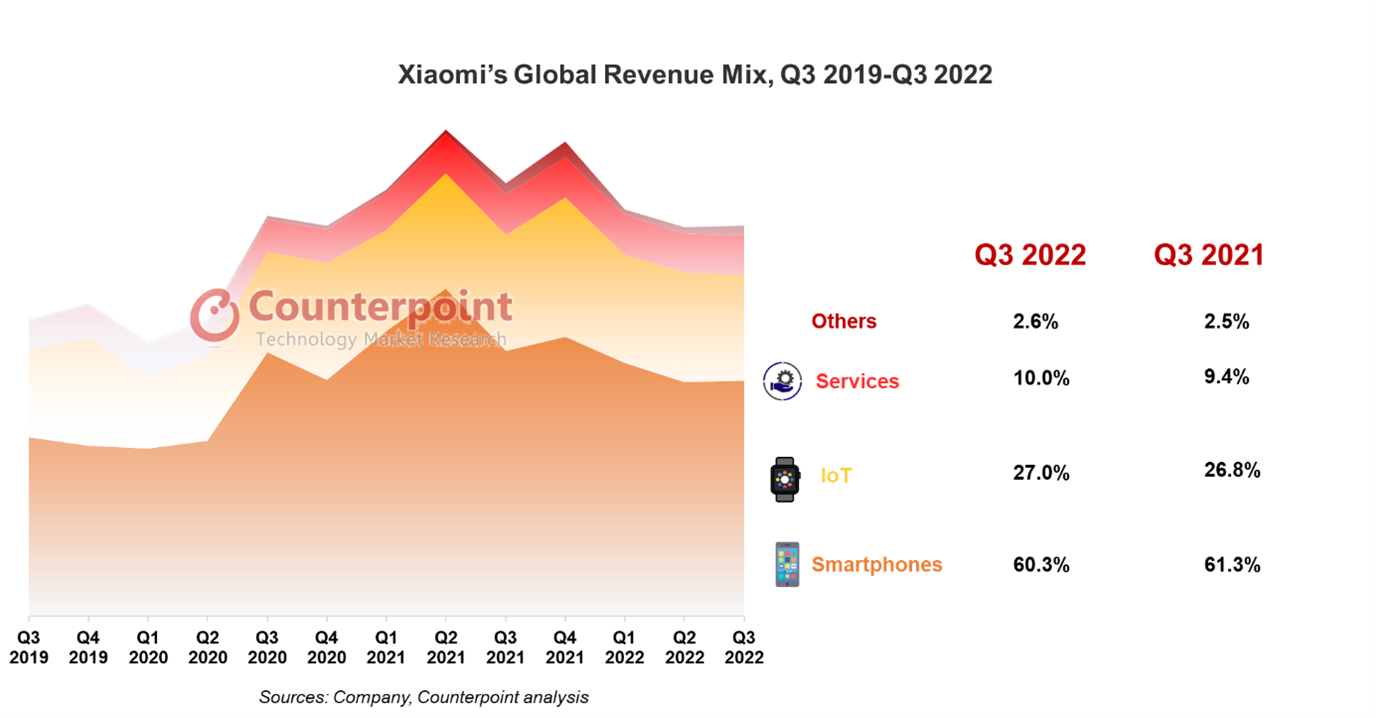

Xiaomi has reported a decline of 9.7% YoY in its Q3 2022 revenue at RMB 70.5 billion (or $9.8 billion). But it stayed largely flat in QoQ terms. The revenue decline was attributed to a slowdown in the company’s three major segments – smartphones, AIoT and internet services.

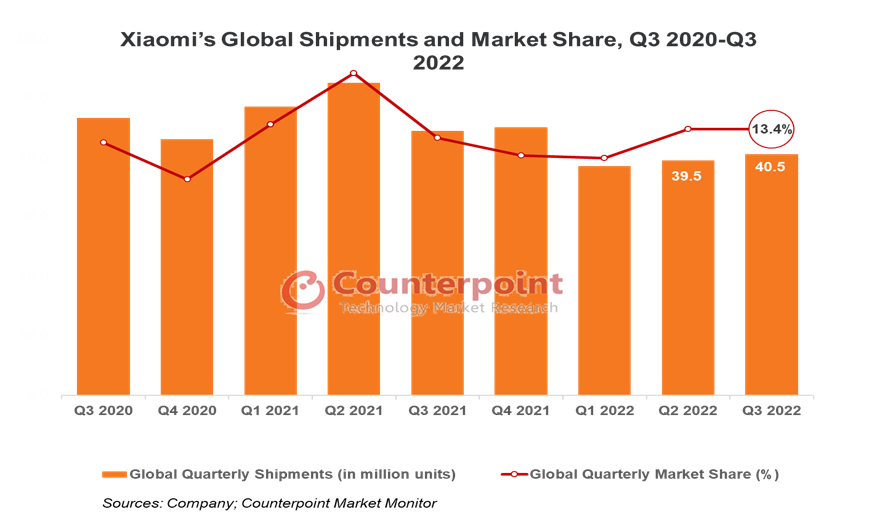

The smartphone segment suffered the most severe decline among the three, with revenue down 11.1% YoY. Based on Counterpoint’s Market Monitor Service, Xiaomi’s shipments were down 8.8% YoY in Q3 2022 with a global market share of 13.4%. The decline in shipments was also accompanied by a decrease in the average selling price (ASP). Xiaomi’s smartphone ASP declined 2.2% QoQ from RMB 1,081.7 (or $ 151) per unit in Q2 to RMB 1,058.2 per unit (or $148) in Q3 due to promotional activities in overseas markets to clear out inventory, offsetting the increase in ASP in China’s market.

The smartphone market continues to face headwinds both in China and globally. In Xiaomi’s home market, ongoing COVID-19 restrictions on mobility and weak economic environment have led to sluggish smartphone sales throughout 2022, which is expected to register a double-digit YoY decline, according to Counterpoint’s estimates. The frequent lockdowns across the country are impacting Xiaomi’s strategy to grow its offline channels, which is seen as a key weakness of the company when compared to OPPO and vivo. Coupled with fierce competition from local players OPPO, vivo and HONOR, as well as Apple’s latest series, Xiaomi’s market position dropped one rank to reach fifth in Q3 2022.

Commenting on Xiaomi’s overseas smartphone business in Q3 2022, Research Analyst Mengmeng Zhang said, “Overseas shipments accounted for more than 75% of Xiaomi’s total shipments. The sluggish macro environment, inflation and foreign exchange fluctuations have also taken a toll on Xiaomi’s sales in the overseas market. On the bright side, we see that Xiaomi is continuously growing its market share in Europe, Latin America and Middle East.”

Xiaomi’s inventory level in China has normalized after the mid-year ‘618’ shopping festival in Q2. However, to clear its inventory for the global market, the company will have to wait till at least Q4, when festive season promotions are launched.

Xiaomi continues to invest heavily in R&D, with the company’s R&D personnel accounting for 48% of its total employees. Xiaomi’s R&D expenditure also grew 25.7% YoY to RMB 4.1 billion (or $0.57 billion) in Q3. More than RMB 829 million (or $116 million) went to new businesses including EV. Xiaomi’s EV business is still in the early stages of development. It is unclear at the moment whether the company will emerge as a leading player in China’s competitive auto market.

Xiaomi’s IoT and lifestyle products segment saw a 9% YoY decline and 4% QoQ decline in Q3. The slowdown in this segment is largely due to weak consumer sentiment. Commenting on the performance of this segment, Senior Analyst Ivan Lam said, “The IoT and lifestyle products remain an important segment for Xiaomi, accounting for 27% of its revenue during the quarter. Despite the segment’s slowing growth, Xiaomi made strong progress in the smart large appliances, such as air conditioners, refrigerators and washing machines, with revenue growing 70% YoY. Smart large appliances are necessities that can better withstand economic downturns. We expect the innovative features of Xiaomi’s smart large appliances to continue to drive demand, especially among younger customers, and become a larger contributor to the IoT and lifestyle products segment.”

Internet services revenue was also muted, declining 3.7% YoY while growing 1.4% QoQ. The segment was particularly hurt by slower China advertisement demand despite growth in overseas markets. Research Analyst Archie Zhang said, “Although the monthly active users of MIUI have reached record highs both globally and in China, monetizing the traffic is challenging during the difficult macro environment and will likely carry through to 2023.”

Xiaomi Q2 2022 Update

Global Smartphone Market Downturn Impacts Xiaomi Numbers

August 23, 2022

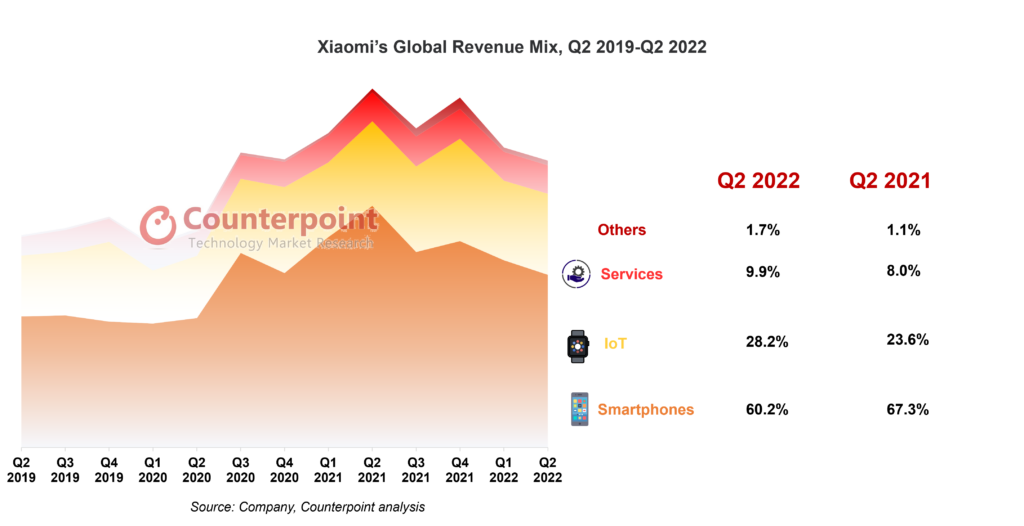

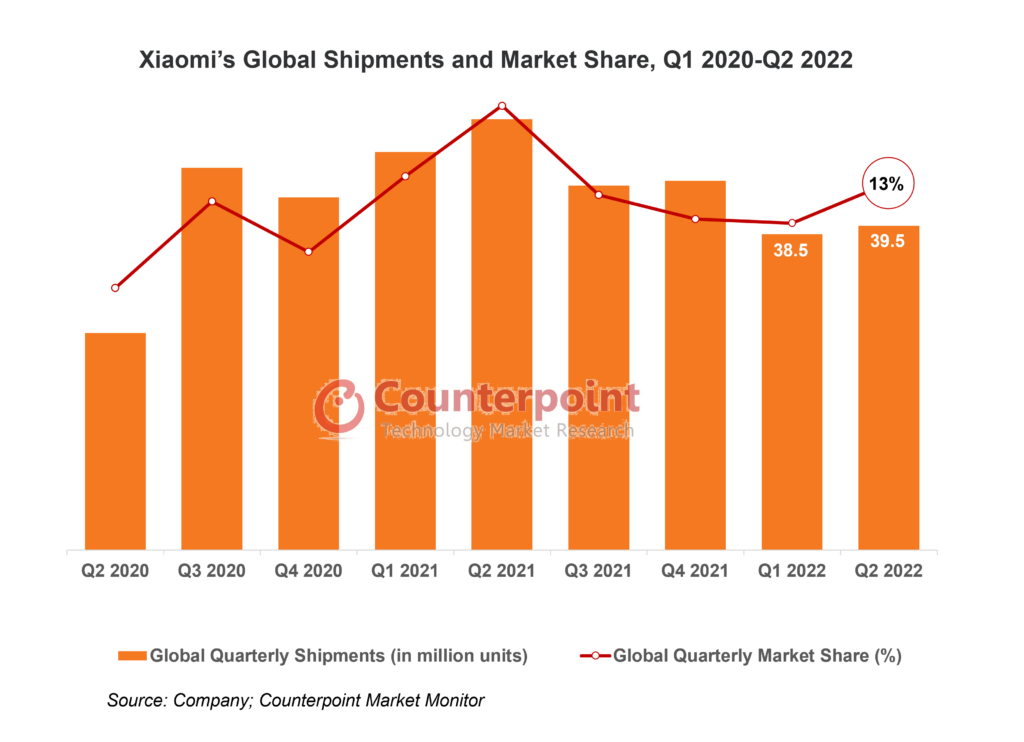

Xiaomi’s latest financial numbers fully demonstrate the impact of the global smartphone market downturn in Q2 2022. The company’s revenue dropped 20.1% YoY to RMB 70.2 billion (or $10.3 billion) during the quarter. Most of this decline came from the company’s smartphone unit, which dropped 28.5% to RMB 42.3 billion ($6.2 billion). According to Counterpoint’s Market Monitor Service, Xiaomi’s shipments were down 25% in Q2 2022 with a market share of 13.4%, the third highest after Apple and Samsung.

Xiaomi’s revenue distribution appeared more diversified in Q2 2022 than it was in the same period last year as the non-smartphone units recorded fewer declines in Q2 2022.

Commenting on Xiaomi’s smartphone business in Q2 2022, Senior Analyst Ivan Lam said, “In Q2, Xiaomi’s smartphone business was squeezed by Samsung overseas and HONOR in home market China. After the mid-year ‘618’ shopping festival, Xiaomi’s inventory situation in China eased and returned to a normal level. However, inventory issues still haunt Xiaomi in other regional markets as global inflation and the looming macroeconomic recession keep customers from purchasing or replacing smartphones. In China, HONOR’s strong momentum also pressured Xiaomi’s smartphone sales in Q2. Xiaomi’s shipment share ranked fourth in China while HONOR took the top spot. Looking forward, we believe the Chinese smartphone market is bottoming out but not before realizing a double-digit decline in 2022. The global market will contract too. Xiaomi is slowing down expansion offline, which will weaken its ability to take on the competition in China. The headwinds faced by Xiaomi’s main business are far from over.”

Inventory issues faced by smartphone OEMs, including Xiaomi, have been under the spotlight this year. There have been reports of OEMs slashing production orders, canceling component purchases and adjusting shipment targets for 2022. According to Counterpoint’s analysis of Xiaomi’s financial report, the company’s inventory turnover days edged higher in Q2 2022. But as the inventory level in China has been lowered, we think Xiaomi may embark on relatively aggressive sales promotion campaigns in other regional markets.

Xiaomi continues to invest in the long term. The company’s R&D expenditure grew 22.8% YoY to RMB 3.8 billion ($0.56 billion) in Q2. More than RMB 611 million went to new businesses including EV.

Founder and CEO Lei Jun said Xiaomi’s EV would go into mass production in the first half of 2024. This means the company still needs one-and-a-half years to see its new growth engine start running. Commenting on Xiaomi’s EV ambition, Research Analyst Archie Zhang said, “EV is a brand-new business for Xiaomi. Therefore, its smartphone business needs to generate enough profits to sustain the growing ADAS and digital cockpit R&D expenditure. Xiaomi has a great advantage over car OEMs, especially since it knows what tech-savvy customers are looking for. But our research shows EV customers still prioritize safety over other factors such as in-car entertainment. That is why established car OEMs like BYD and Volkswagen still dominate EV sales in China, according to our data. Xiaomi may need a couple of more years to prove that its EVs are stable and secure to win over a considerable market share.”

Xiaomi Q1 2022 Update

Xiaomi’s 4.6% YoY Revenue Decrease in Q1 2022 Signals Turbulence in Smartphone Segment

May 23, 2022

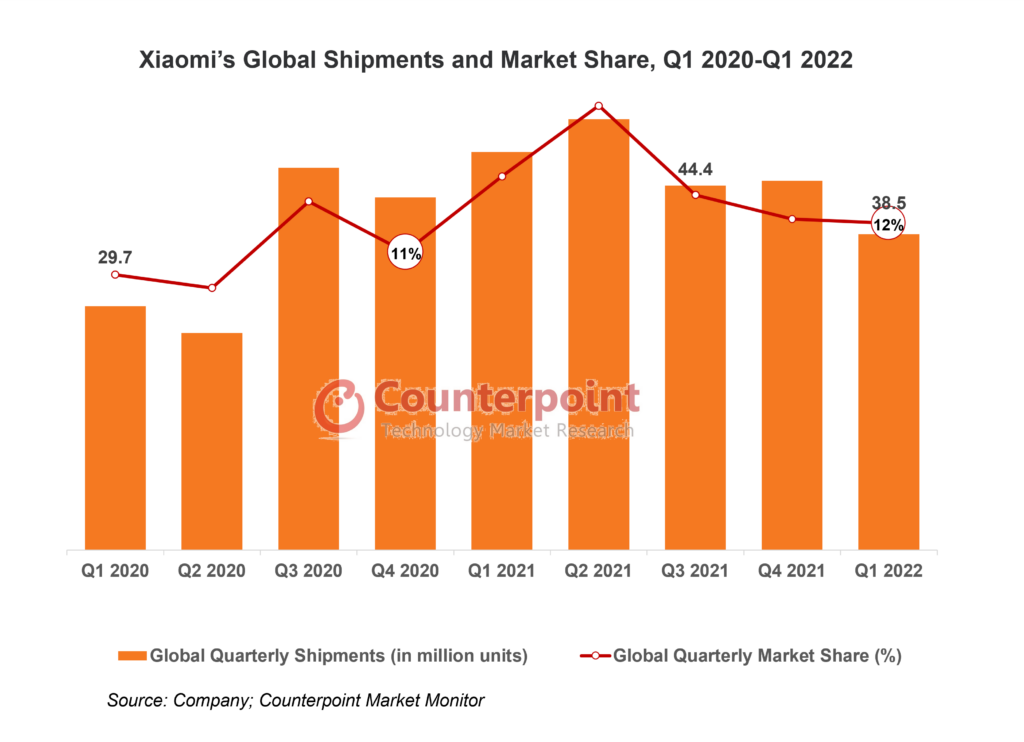

Xiaomi registered a 4.6% YoY and 14.3% QoQ decline in its Q1 2022 revenue, something which was being expected. The result can be mainly attributed to the decline in its smartphone sales globally. The company’s smartphone business, which is its biggest, recorded an 11.1% YoY decline. Xiaomi’s global smartphone shipment share has been declining through the past three quarters, from the highest point of 16% in Q2 2021 to 12% in Q1 2022, according to the latest Counterpoint Market Monitor data. Shipments have hit their lowest point since Q3 2020.

With the ongoing shortages of key components such as 4G SoC, COVID-19 resurgence in some regions, and global macroeconomic headwinds, Xiaomi’s smartphone shipments declined 20.6% YoY in Q1 2022 against the global decline of 8.1% and China market decline of 18.1%, according to Counterpoint’s Market Monitor data.

Commenting on Xiaomi’s smartphone sales, Senior Analyst Ivan Lam said, “Q1 is usually a seasonal low point for all OEMs. But Xiaomi’s smartphone sales declined more than the market. Historically, Xiaomi built its base with entry-level and budget mid-end smartphones such as the Redmi 9A/9C and the Redmi Note series. Therefore, the LTE chipset shortage weighed on Xiaomi’s performance in the lower-end segments. However, we can also see the ASP (average selling price) for Xiaomi’s phones increasing to CNY 1,189 (around $176), which may be the only thing to cheer about in its Q1 2022 numbers.”

Xiaomi’s cost of smartphone sales decreased by 8.1%, primarily due to the reduction in sales, partially offset by an increase in average cost of sales due to a higher proportion of mid-range and premium smartphone shipments. Commenting on the sales activities, Lam said, “Xiaomi had a bumpy ride in its offline channel expansion in China. After spending big amounts along with offline partners, Xiaomi saw no change in its share of offline sales. To make matters worse, Xiaomi now has a high inventory, especially of mid-to-high-end and high-end smartphones. This has pushed Xiaomi to spend more on promotion activities. We observed that its number of inventory turnover days at the end of Q1 2022 was much higher than in Q1 2021. A high inventory is a danger sign for Q2 2022 as COVID-19 lockdowns are on in some major Chinese cities, reducing people’s ability to purchase new smartphones.”

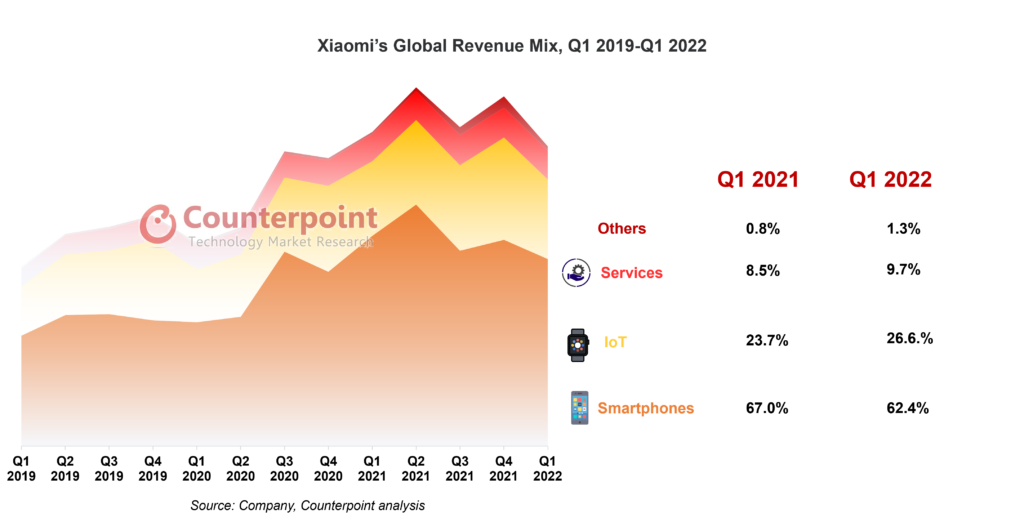

Xiaomi’s IoT and lifestyle products segment saw a 6.8% YoY increase and 22.3% QoQ decrease in Q1 2022. The company’s TV product sales in China lead the show for this segment, retaining the No. 1 spot in the home market for 13 quarters now. Commenting on the performance of this segment, Senior Analyst Yang Wang said, “With 26.6% of the total group revenue, IoT and lifestyle products are a major revenue contributor. However, the segment is not making much money compared to the smartphone segment. And the increase in the profit is mainly attributable to the decreased price of key components such as display panels. In wearable products too, Xiaomi has seen disappointing results. Though it is the leading smartphone brand in India, Xiaomi’s TWS and smartwatch models have not been able to enter the top five brands lists. India’s TWS and smartwatch shipments grew 66% and 173% YoY respectively in Q1 2022 but still, Xiaomi was left out. It could have done better in its second-biggest revenue contributor.”

Xiaomi’s internet services business grew to 9.7% of the company’s total revenue in Q1 2022, registering an 8.2% YoY increase and 2.2% QoQ decrease. The QoQ decrease is due to poor smartphone sales. Commenting on Xiaomi’s internet services segment, Research Analyst Archie Zhang said, “Xiaomi’s internet services segment is continuously bringing positive news against the backdrop of Google grabbing a big portion of such revenue in overseas markets. Xiaomi just passed the 500-million installed base mark to join Samsung and Apple, but it needs to take innovative approaches to monetize the traffic from its products sold overseas.”

In its financial statement, Xiaomi had little information to share on its smart electric vehicle project, the R&D spending on which stands at 12.2% of the overall R&D expense. The statement also mentioned an ongoing investigation by India’s government into some allegations against the company.

Xiaomi Q4 2021 Update

Xiaomi Wraps Up 2021 on a Strong Footing, Despite Challenges

March 23, 2022

With a 9.6% sequential increase in total revenue in Q4 2021, Xiaomi has partially recovered from its underwhelming performance in Q3. In terms of segment performance, its smartphone revenues increased 18.4% YoY. IoT and Lifestyle products and Internet services also saw 19.1% and 17.7% YoY increases respectively.

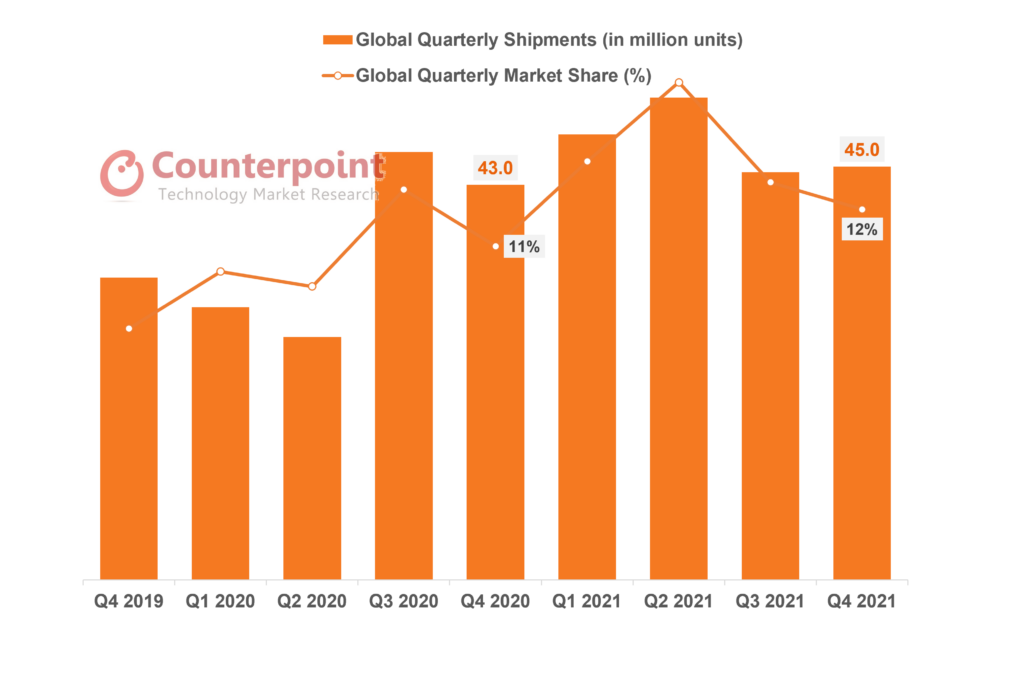

The company’s latest financial data is also in line with Counterpoint’s Market Monitor data, which shows Xiaomi’s smartphone shipments increased 4.7% YoY and 1.4% QoQ in Q4 2021. The slower increase in smartphone shipments growth as compared to revenue growth illustrates that Xiaomi has made fairly good progress upgrading its portfolio and improving its smartphone average selling price (ASP). Correspondingly, Xiaomi’s gross margin from smartphones improved from 8.7% in 2020 to 11.9% in Q4 2021.

Xiaomi’s Global Shipments and Market Share, Q4 2019-Q4 2021

Commenting on Xiaomi’s smartphone sales, Senior Analyst Ivan Lam said, “Counterpoint’s Market Monitor data shows that Xiaomi’s smartphone shipment growth has underperformed the global market total in Q4 2021. Key component shortages, especially in LTE, constrained Xiaomi’s low-end smartphones sales. However, the increase in ASP helped Xiaomi to keep up with revenue growth. The company is moving in the right direction as it has tried to contain the share of entry-level smartphones.”

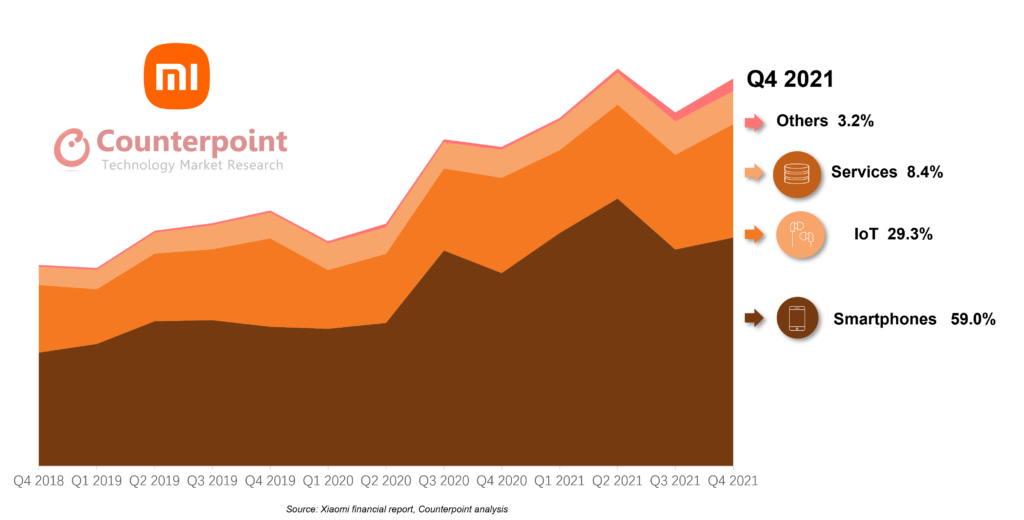

Xiaomi’s IoT and Lifestyle products segment saw record performance in 2021, with revenue coming in at RMB 25 billion in Q4, up 19% YoY. Commenting on the performance of this segment, Senior Analyst Yang Wang said, “IoT and Lifestyle products are becoming more and more important to leading smartphone OEMs. Those products can be sold into the same channels as smartphones in most regions, and can therefore be boosted by the same marketing halo effect, such as bundled sales, promotions and new product launches. Notably, Xiaomi’s TVs, laptops, tablets, wearables, and home appliances saw good sales, due to Xiaomi’s affordable pricing strategy.”

Last but not least, Xiaomi’s internet services revenue reached a record RMB 7.3 billion in Q4 2021, translating into a growth of 17.7% YoY. This was attributed to the advertising business, as well as a 79.5% YoY growth in overseas markets.

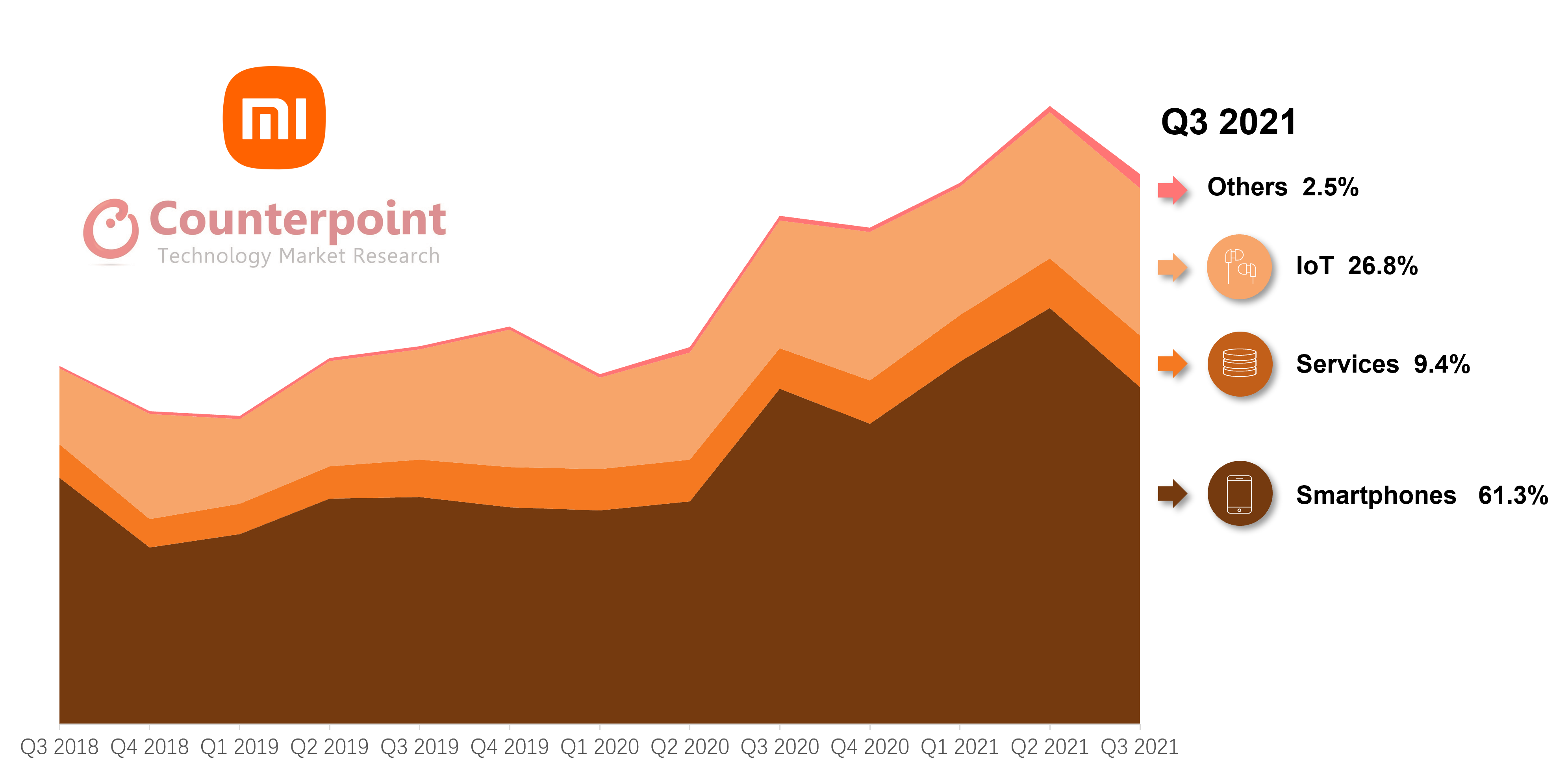

Xiaomi’s Global Revenue Mix and Share, Q4 2018-Q4 2021

During the earnings call, Xiaomi disclosed that revenue from the smartphone segment grew 37%, and was still the biggest contributor to the company in 2021 at 63.6%. Smartphones’ cost of sales remained stable at 56.0% in 2021, as compared to 56.5% in 2020. The cost structure has thus improved by pushing up the ASP.

Internet services made 8.6% of total revenue in 2021. Commenting on Xiaomi’s internet services segment, Research Analyst Archie Zhang said, “Xiaomi’s internet services segment has shown decent growth momentum. Notably, overseas services revenues grew 18.8% YoY in 2021. However, Xiaomi faced several challenges, including more stringent regulations around targeted advertising and privacy, and a weak home market due to sluggish performance of the big internet companies in China.”

Xiaomi closed the buy-out of the 50.09% stake of Zimi International Incorporation that it does not already own. By bringing the ‘ecosystem’ company under its control, Xiaomi can boost its offers in accessories such as mobile power banks, wireless chargers, and smart home accessories. Xiaomi also acquired Deepmotion Tech Limited, a company specializing in advanced driver-assistance systems (ADAS) and automated driving applications. Xiaomi announced that the mass production of its smart electric vehicle will officially begin in the first half of 2024.

Xiaomi Q3 2021 Update

Xiaomi’s Growth Pegged Back by Component Shortages

November 24, 2021

Hit by the ongoing global component shortages, Xiaomi’s smartphone revenues nearly came to a halt in Q3 2021, growing just 0.5% YoY and falling 19% QoQ. Therefore, the strong momentum and fast expansion seen in Xiaomi’s smartphone segment after Huawei’s fall ended after a year. Xiaomi’s internet services segment provided a silver lining but its average revenue per user (ARPU) continued to fall.

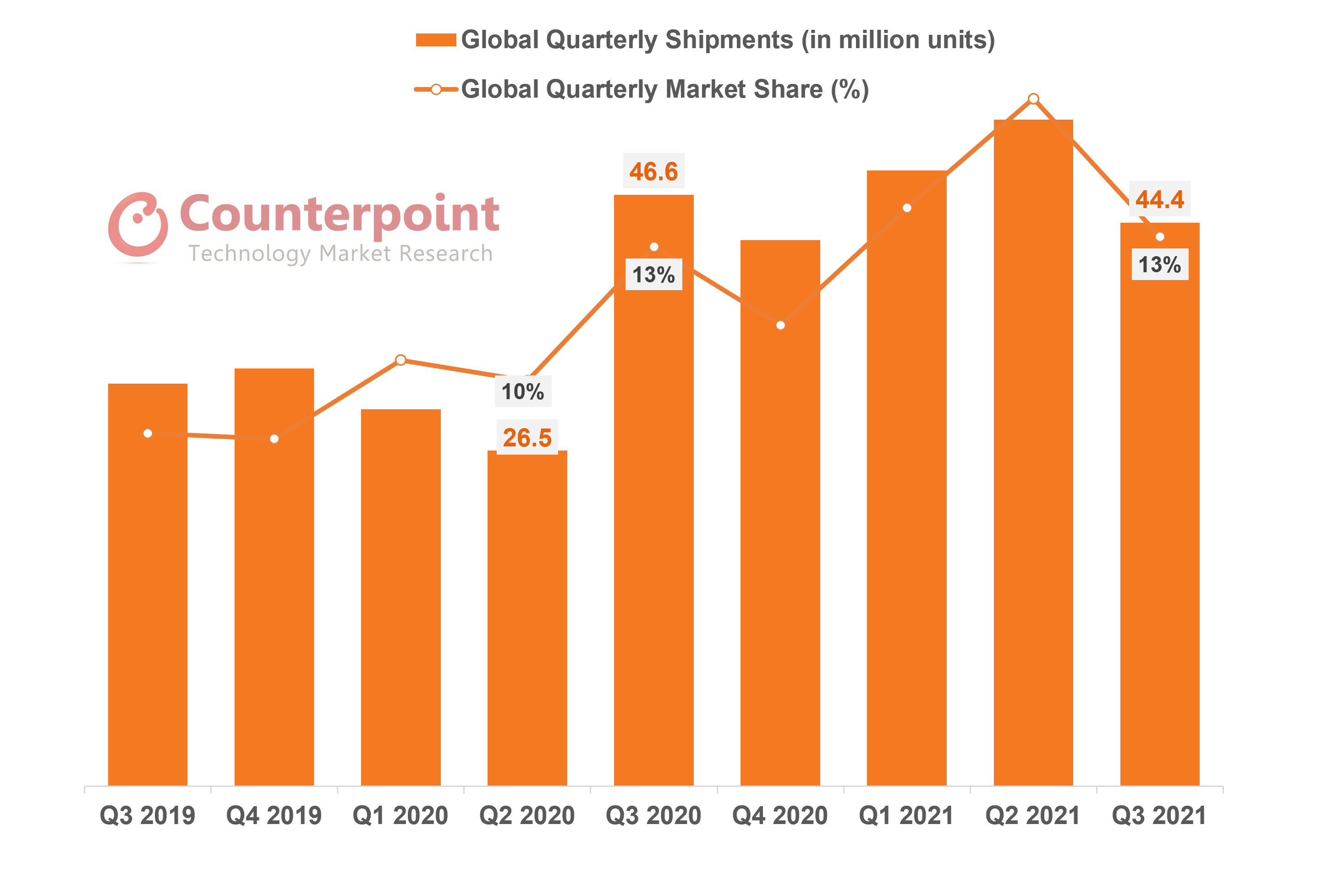

The company’s latest financial data is also in line with Counterpoint’s Market Monitor data, which shows Xiaomi’s smartphone shipments dropping 4.7% YoY and 15.3% QoQ in Q3 2021. The slower decrease in smartphone revenue growth compared to shipments illustrates that Xiaomi made fair progress in improving its smartphone average selling price (ASP).

Xiaomi’s Global Shipments and Market Share, Q3 2019-Q3 2021

Commenting on Xiaomi’s smartphone sales, Senior Analyst Ivan Lam said, “Counterpoint’s Market Monitor data shows that Xiaomi’s smartphone ASP increased more than 7% YoY to $180 in Q3 2021 but dropped about 3% QoQ. The increase in ASP helped Xiaomi to keep revenue flat from the figure of Q3 2020. Since Xiaomi aims to double down on its premium product strategy, we can expect its ASP to continue to increase. On the other hand, component shortages will also play out, especially for Xiaomi products, which boast to have ultra-low profit margins.”

Xiaomi did have some good news in Q3 2021. The company’s internet services revenue reached a record RMB7.3 billion, translating into a growth of 27.1% YoY and 4.3% QoQ, fastest among all segments.

At an earnings call, Xiaomi disclosed that its overseas services revenue accounted for 19.9% of its whole internet services segment. The share was more than 500 basis points higher from the previous quarter.

Commenting on Xiaomi’s internet services segment, Senior Analyst Yang Wang said, “Xiaomi’s internet services segment has shown a great growth momentum. Especially, the overseas services revenue grew more than 110% YoY in Q3 2021. We believe India will continue to be the key growth region. The revenue from mainland China will face more uncertainties given sluggish advertising growth at major internet companies. Xiaomi can partner with these internet companies, providing them key data for ad personalization. We think this downturn in China advertising will reflect in Xiaomi’s earnings in the coming quarters.”

Moreover, Xiaomi’s ARPU has dropped for five quarters to RMB15.1. This has been due to the difficulty in competing against Google in the global market. Xiaomi still can’t commercialize data as efficiently as it does in China.

Xiaomi Q2 2021 Update

Smartphone Sales Soar as Company Reports Best Quarter on Record

September 8, 2021

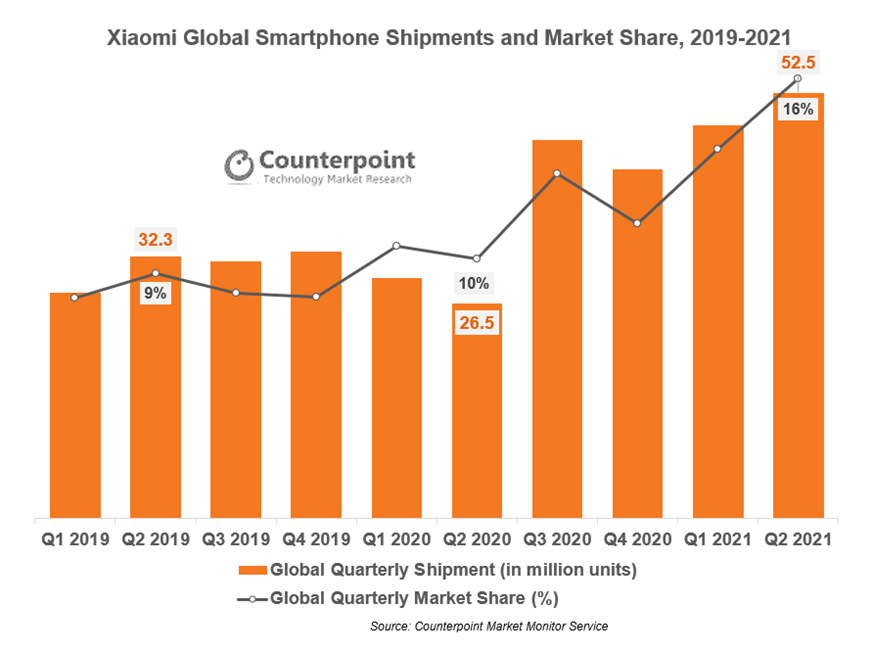

Xiaomi saw a record-setting Q2 2021 with revenues growing 64% and net income surging 80% from the same period a year ago. This performance was driven largely by strong smartphone sales, which reached 52.5 million units in Q2, according to Counterpoint Research’s Market Monitor service.

Smartphone sales growth was broad-based for Xiaomi across most regions. The company has focused on emerging markets such as Southeast Asia, Middle East and Africa, and Latin America, where sales grew 99%, 206% and 229% respectively in YoY terms. Even in the more developed European markets, Xiaomi’s sales grew 109% YoY.

Commenting on Xiaomi’s smartphone product strategy, Senior Analyst Ivan Lam said, “Our numbers show the average selling price (ASP) of Xiaomi phones reached the highest ever at $185 in Q2 2021. This is an increase of 7.3% in YoY terms, driven mainly by the performance of premium products such as the Mi 11 series. We expect Xiaomi to double down on premium segments to uplift its brand in home market China, and high ASP markets like Western Europe, where Huawei’s fall has left a vacuum in the premium range.”

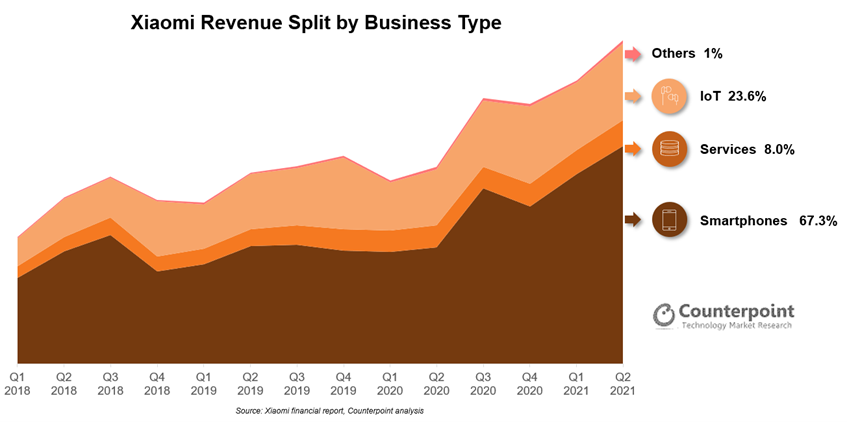

Looking at Xiaomi’s revenue growth by business type, the smartphones, services and IoT segments grew 86.8%, 19,1% and 35.9% respectively in YoY terms. The company’s business is now more than ever dependent on its smartphone segment, which accounts for two-thirds of the total revenue.

Commenting on Xiaomi’s services segment performance, Analyst Archie Zhang said, “While Xiaomi’s smartphone business performed extremely well, there still is a lot of potential to tap into its services segment. During a period when smartphone sales almost doubled, services revenue growth lagged. The average revenue per user (ARPU) in Q2 2021 actually dropped 10% to RMB 15.5, suggesting that monetizing user traffic on smartphones in new geographies is not as straightforward.”

Within Xiaomi’s services segment, advertising revenue was up 46.2%, while gaming revenue dropped 10.7% and value-added services (VAS) revenue dropped 10.3%. Gaming and VAS are likely to face further pressure due to online gaming and financial services regulatory controls in China. Therefore, advertising will become crucial to Xiaomi’s services success, and we expect it to beef up collaborations with leading internet companies and expand partnerships abroad.

Despite these challenges, the services segment’s gross profit margin soared to 74.1% compared to 60.3% a year ago. With a revenue contribution of only 8%, the segment contributed to 35% of the company’s gross profit. Given the company’s stated intention to keep smartphone margins low, we expect services to continue to do the heavy weightlifting for Xiaomi’s bottom line in the future.

* Key Southeast Asia countries include Indonesia Thailand Philippines and Vietnam