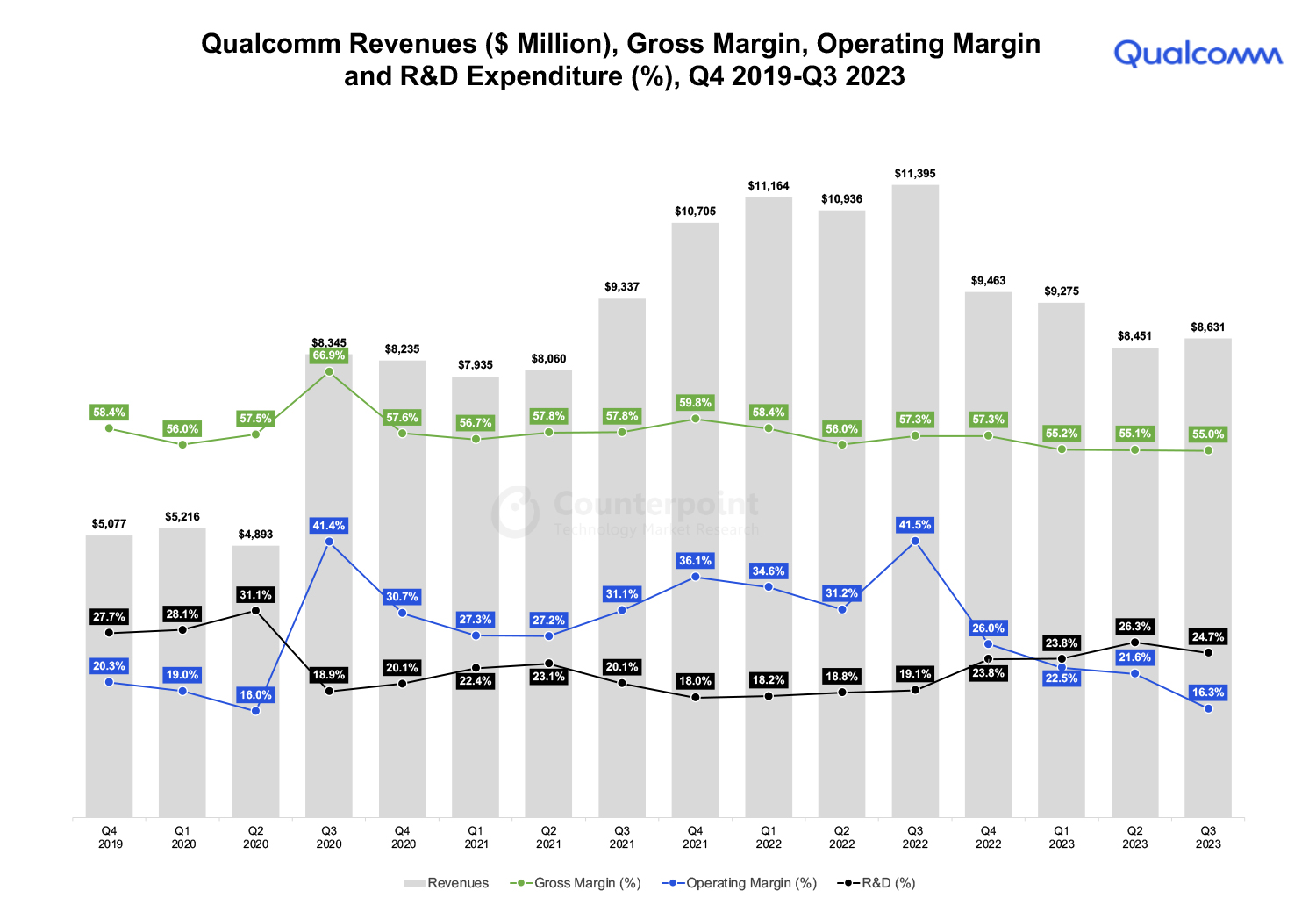

- Total revenues declined by 24% annually in Q3 2023 to reach $8.6 billion. The revenues slightly increased sequentially due to the recovery in the smartphone market and improving channel inventory.

- The company’s handsets business captured revenues of $5.5 billion, declining 27% annually but growing 4% sequentially.

- Overall, we expect the premium handset market to drive revenues for Qualcomm while focusing on mixed shifts toward the low- to mid-end 5G market will drive further growth.

Qualcomm’s total revenue in Q3 2023 declined 24% YoY to reach $8.6 billion. However, the revenue increased slightly QoQ due to recovery in the smartphone market and improving channel inventory. The company’s handset-related business grew 4% sequentially on recovering Android demand.

During the earnings call, Qualcomm CEO Cristiano Renno Amon discussed the company’s performance and outlook on key areas like ARM PC and Huawei comeback.

ARM-based PC opportunity

CEO Cristiano Renno Amon: “…I think Snapdragon X Elite represents the results of this Microsoft-Qualcomm collaboration… if you look at the announcements of other computing companies talking about having an ARM-based PC processor, that is validation that that’s our TAM now. It is going to be part of the expansion of TAM for Qualcomm. We are a new player, and we look at this as a growth opportunity. We are excited about it.”

Analyst take: The AI PC market is witnessing a surge, underpinned by Intel and Qualcomm’s new PC CPU platform, which is just around the corner. These AI-enabled PCs will likely be available around mid-2024. We expect AI PCs to have an over 50% 10-year CAGR from 2020, and after 2026, they will dominate the PC market. Intel, Qualcomm and other PC CPU makers are working closely with PC OEMs for the next-generation mainstream models, marking a new chapter for the PC industry.

Outlook and headwinds

CEO Cristiano Renno Amon: “…as we indicated in the last earnings call, …we don’t have any more projection of selling our 4G… SoCs to Huawei. And going forward, we do not expect (it) to have any significance – it’s going to be a very small contribution from Huawei. I think the more interesting answer to your question, and that’s the reason I provide the 35% data point (QCT handset forecast includes sequential revenue growth of greater than 35% from Chinese OEMs), is as Huawei launched the device, what we are seeing from our customers is …growth… on the Android side. We see a mixed improvement of our customers, moving towards flagship, and it’s kind of reflected in our numbers. So it does not change the trajectory that we have with our Android customers in China. And there is a possibility that Huawei is upgrading its existing customer base. There was a data point – there are about 100 million Huawei former customers with a 4- to 5-year-old Huawei phone, and that could have an impact on increasing the TAM.”

Analyst take: Qualcomm did not consider any material revenues from Huawei due to Huawei’s in-house chipset adoption. Huawei’s aggressive comeback will increase competition in the Chinese market and affect the overall 5G TAM. However, sequential revenue growth from Chinese OEMs and increased silicon content because of AI adoption will have a positive impact on the blended ASP and units.

CEO Cristiano Renno Amon: “…in fiscal ’23 that just ended, we had a share increase both globally and in China of sell-through. And we like, I think, the direction that we have been going …as we said, we will continue to retain a majority share at Samsung. We feel good about that relationship going forward. And we have seen traction from premium and high-tier Chinese OEMs. This is in spite of the launch of and the successful initial sales of a newcomer. And that’s kind of also reflected in the sequential 35% growth.”

Analyst take: With the launch of the Exynos 2400, Samsung may adopt an in-house chipset in its Galaxy S series. However, Qualcomm has highlighted it will have the majority share in the Samsung flagship. Based on our smartphone sell-through tracker, Qualcomm leads the Chinese market and has increased its share in the past few quarters. Overall, we expect the premium market to drive revenues for Qualcomm while focusing on mixed shifts toward the low- to mid-end 5G market will drive further growth.

Results summary

- Signs of recovery: Total revenues declined by 24% annually in Q3 2023 to reach $8.6 billion. The revenues slightly increased sequentially due to the recovery in the smartphone market and improving channel inventory.

- Handset revenues increased sequentially: The company’s handsets business captured revenues of $5.5 billion, declining 27% annually. The segment grew 4% sequentially due to the early stages of recovery in Android demand.

- IoT revenues decline: IoT revenues were recorded at $1.4 billion, declining 7% sequentially due to the weak demand from industrial IoT customers and inventory drawdown.

- Auto revenues: Auto revenues in Q3 2023 grew 23% sequentially to reach $535 million. The company has expanded its auto platform by entering two-wheelers and having design wins with Gogoro, Harley-Davidson and others. Qualcomm has also entered into a strategic partnership with AWS to integrate cloud and AI into vehicle development.

- Agreement with Apple: Apple and Qualcomm have reached an agreement to supply Snapdragon 5G Modem-RF systems for smartphone launches in 2024, 2025 and 2026, reinforcing their ongoing relationship. The iPhone model launched in 2026 will have a 20% Qualcomm baseband share.

- Inventory turnover: Inventory levels are coming down to a normal level. We expect the overall inventory environment to reach normal levels by the end of Q1 2024.

- Positive outlook for Q4 due to seasonality: For Q4 2023, Qualcomm guided revenues to be between $9.1 billion and $9.9 billion, growing 5%-15% sequentially. The company forecasted a sequential double-digit growth in handset revenues in Q4 2023, driven by launches in the premium segment and seasonality.