- Growth comes in a year that is seeing multiple macroeconomic headwinds.

- With its big win at Samsung, Qualcomm’s share in the Galaxy S flagship for 2023 will grow to 100%.

- Qualcomm has extended its license with Apple. It will now supply most of the modems to iPhones in 2023.

- H1 2023 will be weak, but Qualcomm has strong fundamentals for long-term growth.

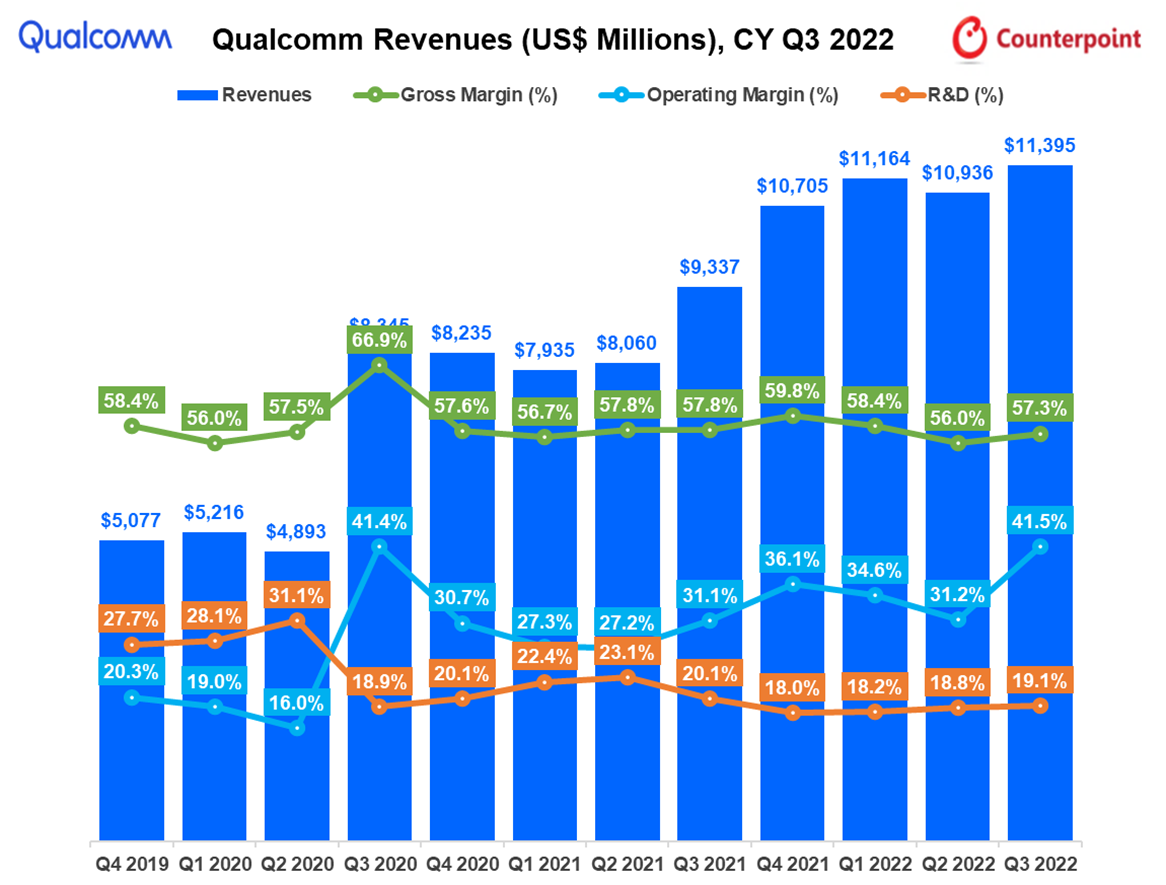

Qualcomm has reported record revenues for its July-September quarter, which is also the last quarter of its financial year. The top line grew 22% YoY to $11.4 billion. This growth comes in a year that is seeing multiple macroeconomic headwinds, with most semiconductor companies struggling with weakening consumer sentiment. Qualcomm has been somewhat immune to this due to its growing business diversification beyond smartphones, like in IoT (FWA, Windows on Snapdragon, industrial IoT and Connected edge) and automotive. Within smartphones as well, Qualcomm’s strategy to focus on the premium 5G segment and increase the share of semiconductor content from SoC to RFFE has helped the company register some growth even though the overall smartphone demand has been softening.

The outlook for the next financial year remains weak due to the ongoing macroeconomic turbulence, prolonged Russia-Ukraine war, energy crisis, rising inflation, China’s COVID-19 restrictions and market exiting with higher-than-normal channel inventories. As a result, despite a strong performance, Qualcomm, going forward, is focusing on prudently managing operating expenses, freezing hiring, reducing expenditure in matured product areas and optimizing selling, general and administrative expenses (SG&A) for targeted R&D investment in growth areas such as automotive and IoT.

Sources: Qualcomm, Counterpoint Semiconductor Tracker

July-September Quarter Analysis:

- In Q3 CY2022, Qualcomm’s recorded revenues grew 22% YoY to reach $11.4 billion.

- QCT (chipset) business revenue increased 28% YoY to an all-time high of $9.9 billion, while QTL (licensing) business revenue declined 8% YoY to $1.4 billion due to weaker smartphone unit sales resulting in lesser royalties.

- Within QCT, handset segment revenues reached $6.6 billion, growing 40% YoY. Handsets contributed around 66% of the total QCT revenues. The smartphone SoC shipments were driven by strong adoption of the flagship Snapdragon 8 Gen 1 and Snapdragon 778G series in the premium and high-end segments respectively.

- IoT revenues were up 24% YoY to reach $1.9 billion in Q3 CY2022 driven by edge networking and industrial IoT. Qualcomm signed a multi-year agreement with Meta for AR/VR on Snapdragon chipsets. Meta’s Quest Pro has three chipsets from Qualcomm – Snapdragon XR 2+ in the headset and two Snapdragon 662 in the controllers. This is a significant win in the Meta Quest Pro Bill of Materials (BoM)

- Strong traction from the Wi-Fi 6/6E solution, next-gen Wi-Fi 7 solution, 5G FWA and Windows on Snapdragon, Robotics, and edge processing will drive the overall IoT revenues going forward.

- Auto revenues reached $0.4 billion, growing 58% YoY driven by Snapdragon Digital Chassis. Qualcomm has an auto design win pipeline across connectivity, digital cockpit and ADAS worth over $30 billion. This shows Qualcomm’s diversification is working and will be a big revenue stream going forward.

- RFFE revenues declined 20% YoY to reach $992 million due to the continued weakness of the handset market and channel inventory. According to Counterpoint’s Smartphone RFFE Revenue Tracker, the 2022 growth forecast for the smartphone RFFE market has been revised to the low single-digit range (1%~3%) to reflect the greater-than-expected impact on demand for RFFE components. Qualcomm, which is already a leader in smartphone RFFE, has designed a win pipeline of greater than $900 million in auto and $405 million in revenues within IoT.

Outlook

- In the lucrative 5G discrete baseband modem business, Qualcomm has extended its license with Apple and will be supplying most of the modems to new iPhones launching in 2023 with sales continuing through 2024.

- Beyond 2024, the contribution from Apple will be subject to how successful Apple is in building its first baseband capability, either integrated within SoC or discrete. So far, it has been a struggle to build its first in-house modem capabilities.

- Another big win is with Samsung as the share of Qualcomm solutions within the Galaxy S series flagship for 2023 will grow to 100% from 75% in the Galaxy S22. The fact that the world’s leading and vertically integrated Android vendor has chosen Qualcomm’s Snapdragon flagship SoC for its flagship models, from the S series to foldable, shows how Qualcomm is dominating the premium smartphone segment with its SoC capabilities.

- As we have highlighted before, it is difficult to develop an end-to-end smartphone solution from SoC to RFFE. Qualcomm, with its forward integration capabilities, is the only game in town when it comes to high-to-premium-tier solutions. The entry of MediaTek’s 9200 will ignite some competition but the performance and capabilities remain to be seen as Qualcomm is generations ahead when it comes to AI, camera, 5G baseband, RFFE and so forth.

- Qualcomm’s guidance for Q4 CY2022 forecasts $9.2 billion to $10 billion revenue, non-GAAP EPS of $2.25 to $2.45, QCT revenues at $7.7 billion to $8.3 billion and EBT margins of 26% to 28%, and QTL revenues of $1.45 billion to $1.65 billion. Both the handset and IoT revenue streams are expected to be down sequentially.

- There is 8-10 weeks of elevated inventory in the channel, which will take a couple of quarters to come down. Qualcomm also pointed out inventory correction in the premium segment as well as smartphone OEMs undergoing correction. But the overall impact of the Samsung Galaxy S series win will not be significant as China’s market remains weak.

- Qualcomm’s financial year has been impacted by macroeconomic headwinds and extended China COVID-19 restrictions. This has resulted in demand weakness and temporarily elevated channel inventory across the industry.

Overall, the inventory correction will take two quarters. H1 2023 will be weak, something that has also been pointed out by other semiconductor vendors. A cautious approach is needed for CY2023 due to the weak macroeconomic situation, which is more of a cyclical adjustment. Qualcomm has strong fundamentals for long-term growth. Its design wins are growing for both the auto and IoT segments. The diversification strategy will help the company drive long-term growth